Secure

Your Future

Protecting Your Loved Ones with Reliable

Life Insurance Solutions

What is Permanent Life Insurance

Permanent life insurance is a flexible, guaranteed product that helps ensure the financial security of your loved ones by covering insurance needs such as:

-Bequests to your heirs

-Estate tax management

Expenses related to death and financial obligations

Continuity of your business

Protection for your investments

Permanent life insurance is different from term life insurance in that it offers additional benefits, such as a guaranteed surrender value and the option of paid-up insurance.

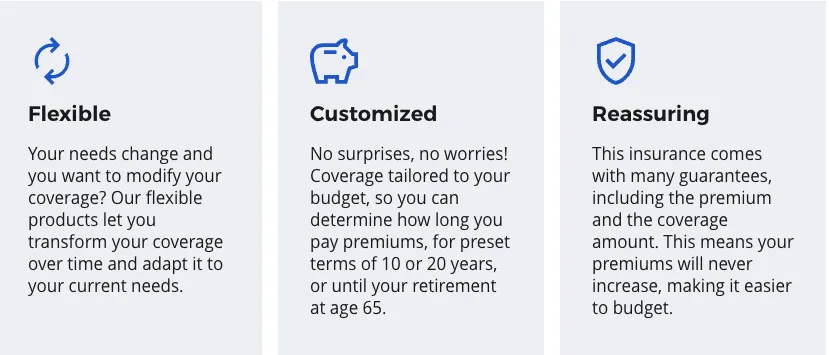

Benefits of permanent life insurance coverage

Protections adapted to your needs

Luke, age 26

Programmer

male, non-smoker

L65 Whole life Insurance

Amount of insurance gauranteed for life:

$200,000

Luke, a bachelor with a new degree in game design, has decided to start his own business. He understands the challenges of entrepreneurship and the importance of planning for the future. He’s looking for a life insurance policy that can guarantee him a lifetime face amount.

Premium

$124.38 / month*

up to age 65

Guaranteed surrender value:

After 20 years: $10,000

At age 65: $56,520

At age 85: $126,380

Mary, age 35

New to Canada

Female, non smoker

Access Life L100 Simplified Issue Life Insurance

Amount of insurance gauranteed for life:

$200,000

Mary recently immigrated to Canada with her family. She is looking for additional life insurance that will provide her and her family with adequate coverage to pay for funeral expenses in her native country in the event of her death.

Premium

$36.50 / month*

$0 thereafter

Guaranteed surrender value:

After 20 years: $3,750

At age 65: $9,245

At age 85: $25,900

**illustration only, rates are subject to change and may not reflect your exact situation

What is the average cost of permanent life insurance?

Permanent life insurance is more expensive than term coverage because it lasts a lifetime and builds cash value. On average, a healthy person in their 30s might pay around $150–$250 per month for $100,000 of coverage. Costs increase with age, health conditions, and higher coverage amounts.

What are the features of permanent life insurance?

Permanent life insurance provides lifetime coverage with fixed premiums that never increase. It also includes a cash value component that grows over time, which you can borrow against or use for future needs. Many people choose it for estate planning, leaving an inheritance, or covering final expenses, since it guarantees a payout as long as premiums are paid.

Who can take out permanent life insurance?

Almost anyone can apply for permanent life insurance, from young adults to seniors. It’s often chosen by people who want lifetime protection, are planning their estate, or want to leave an inheritance. Approval depends on age, health, and the type of permanent policy you apply for, but there are options available for most life stages.

Is it advantageous to convert term life insurance to permanent life insurance?

Yes, it can be. Converting lets you keep coverage for life without going through a new medical exam, even if your health has changed. It’s useful if you want to lock in lifetime protection, build cash value, or use insurance for estate planning. Keep in mind, permanent policies cost more, so it’s best for people who want long-term security and can budget for higher premiums.

What are the benefits of a cash surrender value?

The cash surrender value in permanent life insurance is the savings component you can access while still alive. It grows tax-deferred and can be borrowed against, used to pay premiums, or withdrawn if you no longer need the coverage. This flexibility makes permanent insurance more than just protection — it can also serve as a financial resource during your lifetime.

Do I need permanent life insurance even if I'm single and have no dependents?

Not always. If no one relies on your income, you may not need much coverage. However, permanent life insurance can still be useful to cover final expenses, leave a tax-free gift to family or charity, or lock in coverage while you’re young and healthy. It also builds cash value, which you can access later in life.

Which permanent life insurance coverage do I need?

The right permanent life insurance depends on your goals. Whole life is best if you want guaranteed lifelong protection with stable premiums and a cash value that grows over time. Universal life offers more flexibility, letting you adjust your premiums and death benefit while also building savings. Your choice depends on whether you value predictability, flexibility, or building long-term wealth.

Who do I contact if I want to take out a permanent life insurance policy?

You should contact a licensed life insurance advisor. At LifeAdvisor.ca, I work with CF Canada Financial and top insurance providers to help you find the right permanent policy for your needs. Simply reach out to me for a free one-on-one conversation, and I’ll walk you through your options and the application process.

Contact Us

Alex Lam CF Financial

(778) 898-2539

880 5951 No. 3 Road , Richmond BC V6X 2E3